Sell Car With Loan or Lien in Tennessee

Looking up vehicle information...

Thank You!

Your information has been submitted successfully. Our team will contact you shortly with an offer.

Yes, you can sell a car you still owe money on

01

02

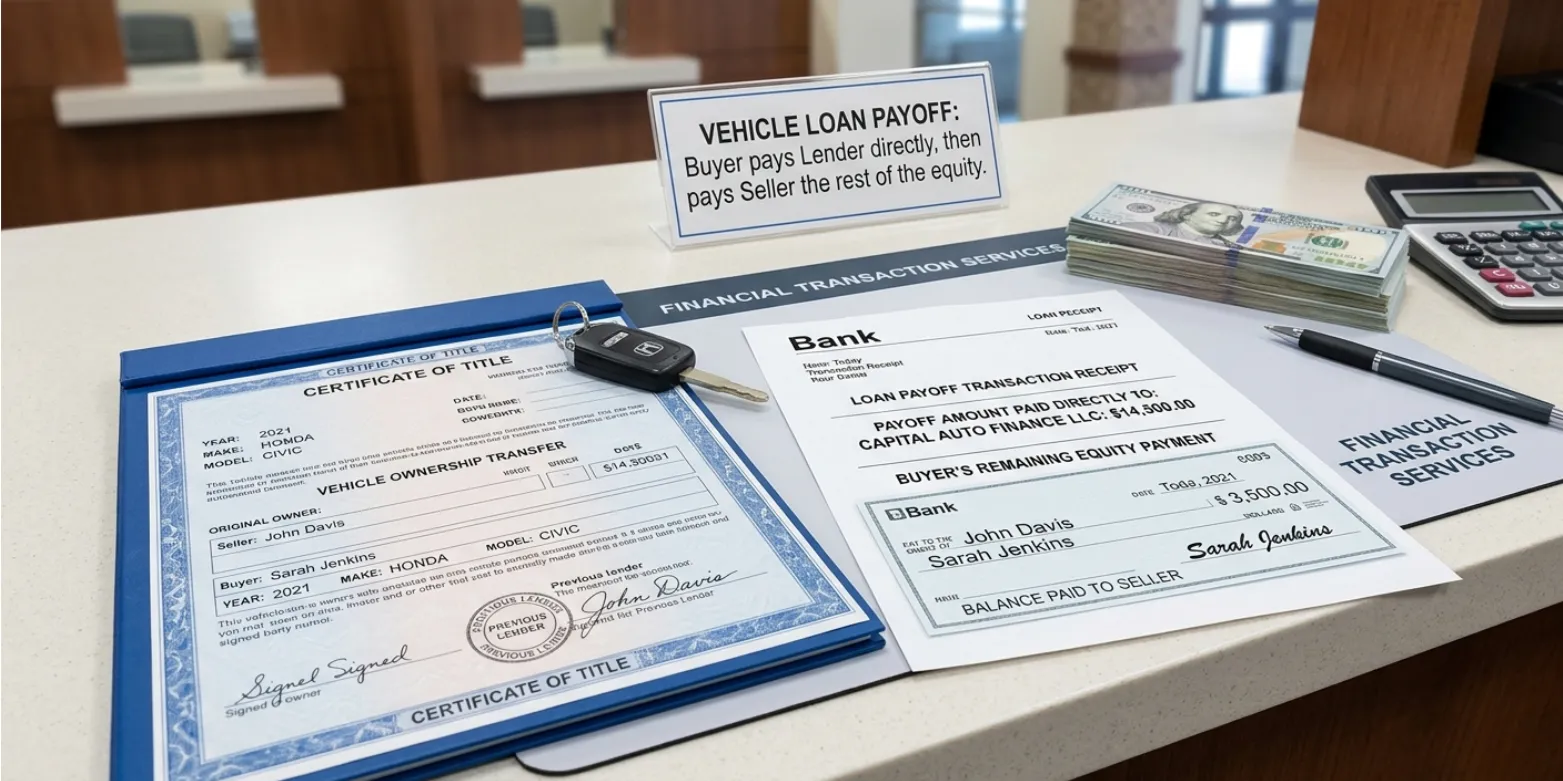

Most private sellers can't pull off option 2 because most private buyers won't trust the process. Option 1 ties up your cash for weeks waiting on the title. Option 3 is the reason we exist.

How lien payoff works in Tennessee

Step 1

Get your 10-day payoff amount from the lender

Bring this number with you. Don't guess — even being $50 short means the lien doesn't release.

Step 2

Buyer pays the lender (or pays you the surplus)

At MCA Direct, we issue one check or ACH directly to your lender for the payoff amount, and a second

payment to you for the difference between our offer and the payoff. Both happen the same day.

Step 3

Lender releases the title to the new owner

You're done the moment you sign the bill of sale and walk out with your check. The title chase is on us.

Three Scenarios Positive Equity, Break-Even, and Upside Down

Scenario 1

you owe less than it's worth (Positive equity)

Example Calculation

MCA Direct's offer:

$18,500

Your 10-day payoff:

$18,500

Your check at closing:

$18,500

Example Calculation

MCA Direct's offer:

$14,500

Your 10-day payoff:

-$14,400

Your check at closing:

$100

Scenario 2

you owe exactly what it's worth (Break-even)

Scenario 3

you owe more than it's worth (Upside down / negative equity)

Example Calculation

MCA Direct's offer:

$12,000

Your 10-day payoff:

-$14,800

You owe at closing:

$2,800

You have three options:

Bring the $2,800 in cash or a cashier's check to close.

The car is gone, the loan is gone, you move on.

Roll the $2,800 into a new auto loan

if you're financing a replacement vehicle.

Wait. Make payments until the loan amortizes below market value.

(Calculate carefully — sometimes the depreciation outpaces the loan payoff and the gap widens.)

We'll tell you exactly where you stand when we make your offer, so there are no surprises at closing.

The Process

How MCA Direct handles loan payoff for you

Fast Turnaround

Total time on your end: about 30 minutes once you arrive.

You submit our form or call (615) 392-6540 with the basics — year, make, model, mileage, condition, ZIP. Tell us there's a loan; we'll factor it in.

We make a real offer based on wholesale market data. The offer is what we pay for the car — independent of what you owe. Your loan situation doesn't change the offer; it changes how we structure the payment.

You call your lender for the 10-day payoff amount.

You bring the car, your loan information, and ID to our Madison location (or schedule pickup).

We verify the payoff with your lender directly.

We issue payment to your lender. We issue your equity check (or collect any negative equity from you).

You sign the bill of sale and the title-release authorization. You walk out free of the loan.

We chase the released title from your lender. You're done.

Documents you need

01

Driver's license (valid, not expired)

02

Current vehicle registration

03

Latest loan statement (paper or screenshot from app)

04

Lender contact info

customer service phone number, payoff fax/email, and your loan account number

05

10-day payoff letter (some lenders provide not always required)

06

Both keys / fobs and remote(s)

07

Owner's manual (if you have it)

08

Service records (helps the offer)

You do NOT need:

the title (your lender has it) a notarized bill of sale (we handle) a release-of-lien letter (we get it from the lender)

Selling a car with a loan in Madison, Hendersonville, Gallatin, and across Middle TN

If you're outside Madison, we offer free local pickup throughout:

Frequently Asked Questions

Q: Can I sell my car in Tennessee if I still owe money on it?

Q: What is a 10-day payoff?

Q: What if I owe more than my car is worth?

Q: How long does lien release take?

Q: Can I sell a leased vehicle this way?

Q: What documents do I need?

Q: Will MCA Direct's offer go down because there's a loan?

Q: What if my lender doesn't release the title for weeks?

Get a cash offer that already accounts for your loan.

Don’t pay off the loan first. Don’t try to coordinate a private buyer with your lender’s title department. Sell to MCA Direct and we handle the entire chain.